Trust us to provide expert IT and cybersecurity solutions. Call us at 339-364-4790 for a free consultation.

Trust us to provide expert IT and cybersecurity solutions. Call us at 339-364-4790 for a free consultation.

Download a Free PDF of this article to share with your leadership team

Download a Free Business Insurance Preparation Checklist to get the best rates possible.

Small to Medium Businesses (SMB) face a myriad of risks that can jeopardize their financial stability and reputation. One critical strategy to mitigate these risks is obtaining commercial general liability (CGL) insurance, errors and omissions (E&O) insurance, and cyber liability insurance. And though there is always the option of being ‘self-insured’, most businesses cannot afford this. This article explores the importance of liability insurance, the key players in the process, the benefits it brings, and how to ensure you pass the underwriting!

Understanding CGL, E&O, and Cyber Insurance

Depending on your industry and risk appetite, your company may be best protected by obtaining one, two, or all three of these insurances!

Why is Liability Insurance a Must Have?

The Section of Doom and Gloom

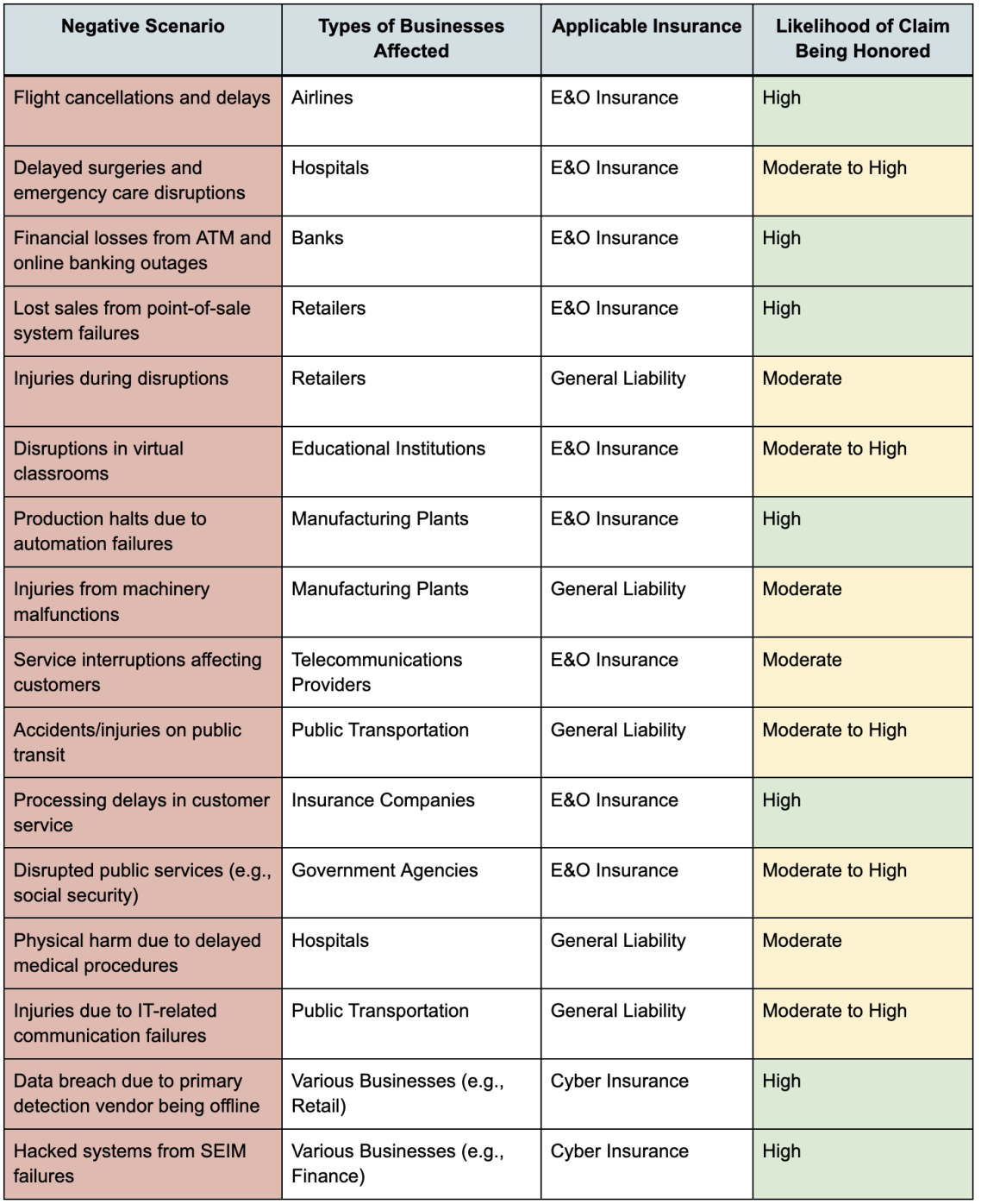

OK, look, it’s hard to get any interest in appreciating risk if you don’t already have a taste of it. In light of the recent global IT outage, companies affected may be able to file claims if they have the correct insurance in place.

Here are a few examples:

Place yourself in the shoes of these business owners…

Cost-Effectiveness and Long-Term Savings

No doubt when you reviewed the scenarios mentioned above, something probably came to mind about your own business and inherent risks that may require further protection. While the cost of liability insurance is an additional expense, it is a worthwhile investment compared to the potentially devastating costs of a liability claim. The premiums paid for insurance can save businesses from significant out-of-pocket expenses and ensure long-term financial stability.

Who Are the Key Players in the Insurance Industry?

How Do You Get Started with Liability Insurance

What’s Required to be Underwritten?

Proof! Proof that you are a low-risk investment for the insurance company. To provide this proof you’ll need to produce quite a few documents as part of the application process. Things like…

Will I Be Audited By the Insurance Company?

Perhaps! Insurers conduct audits to verify that the insured is adhering to the agreed-upon risk management practices and policies, which in turn helps in accurately assessing and managing the risk. You could be subjected to an ‘underwriting audit’, which is typically conducted under the following conditions:

And What if I Have a Claim, Will It Be Paid?

It ‘should’ be as long as your company has been following all of the documentation you provided up-front in the application process. For example, from an insurance perspective, if you are not in compliance with your Information Systems (IS) policies and procedures, several consequences can arise:

Staying compliant with IS policies and procedures is key. Regular internal audits, employee training, and policy updates help maintain compliance and reduce these risks.

It’s a Package!

I've filled out loads of these applications, and it’s a hassle, especially if you're starting from scratch with policies and procedures. But here's the upside: going through this process makes your company stronger and more secure. Getting the right insurance coverage means you’re better protected against cybercrime and financial disasters. Without insurance, legal fees, settlements, and damages could be crippling. Liability, cyber, intellectual property, and product liability insurance all help manage financial fallout and protect your business. It all starts with a thorough analysis of your current state—the good, the bad, and the ugly.

Ever wondered how liability insurance can save your business from financial disaster? From flight cancellations to data breaches, discover how General Liability, Errors & Omissions, and Cyber Insurance protect against unexpected risks.

Learn why every SMB needs these coverages, the role of each insurance type, and real-world scenarios showing their importance. Essential tips for securing the right insurance and maintaining compliance to keep your business safe and thriving!

Download a Free PDF of this article to share with your leadership team

Download a Free Business Insurance Preparation Checklist to get the best rates possible.

Don't know where to start? That's perfectly fine! Reach out for a free consultation, and let's map out a tech strategy that aligns with your objectives. Call us at 339.364.4790 contact@tronpilottech.com

©Copyright 2024. Tronpilot Technologies LLC. All rights reserved.

We need your consent to load the translations

We use a third-party service to translate the website content that may collect data about your activity. Please review the details in the privacy policy and accept the service to view the translations.